The Banking Funnel

With the monetary policy committee (MPC) of RBI meeting between 4th to 6th August and a fresh wave of sanctions from Trump there is a lot of chatter on what stance would be taken going ahead. Even though there is a large focus on the repo rate changes which the central banks propose there are still very different tacit approaches by which the liquidity in economy is controlled. There are controls not only on the credit disbursed but where the credit is being disbursed.

This post is a short understanding of what part of equity and deposits the bank is able to lend out as loans and how different regulations reduce the available credit in the economy. This would be helpful to any one who is reading the financial statements of banks and trying to make sense of it.

Reserve Requirements

First we will look at capital requirements which Banks have to keep to function under duress (that is in event of a bank run). In India this is in the form of -

Cash Reserve Ratio (CRR) — Banks must maintain a certain percentage of Net Demand and Time Liabilities (NDTL) with RBI in cash. This portion earns no interest and cannot be used for lending. As of today the CRR is 4.00%. Statutory Liquidity Ratio (SLR) — Banks need to maintain a certain percentage of NDTL in form of liquid assets like cash, gold and approved sovereign bonds. The amount held in sovereign bonds earns interest but is not available freely for lending. As of today SLR is 18.00%.

Equity Capital Requirements

The next form of capital which gets locked up for the bank is in the form of the Capital Adequacy Ratio (CAR) & Capital Conservation Buffer which is funds tied up for every 100 INR lent. CAR restricts the extent of lending relative to the banks capital base. This is part of the Basel forms put in force after the 2008 Financial crisis.

CAR consists of Tier 1 + Tier 2 capital →

Tier 1 Capital — Core capital of bank, which is strongest buffer against losses. Consists of Paid up Equity Capital, Statutory Reserves, Retained Earnings & instruments as per RBI guidelines Perpetual non-cumulative preference shares & perpetual debt instruments. Tier 2 Capital — Secondary capital to absorb losses but is less permanent and lower in quality. Consists of Subordinated debt, General Provisions and Loan loss reserves. CAR = [Tier 1 Capital + Tier 2 Capital / Risk Weighted Assets (RWAs)] *100

Different type of Assets or loans get different weights as per the risk they carry and is also pre-decided by RBI.

0%: Cash, government securities. 50%: Housing loans (Loan To Value Ratio <= 75%). 75%: Housing loans (Loan To Value Ratio <= 75% and above Rs.30 lakh). 100%: Business loans, some NBFC loans (depending on rating), and some microfinance loans (depending on whether they are considered consumer credit). 125%: Unsecured retail loans, some microfinance loans (depending on whether they are considered consumer credit), and some NBFC loans (depending on rating). 150%: Some NBFC loans (depending on rating) and credit card receivables It is difficult for the bank now to give more unsecured retail loans and credit card receivables which RBI observed were increasing very rapidly and can cause the people to get in a debt trap.

CET 1 is a subset of Tier 1 capital and is of the highest quality which means it does not even include the perpetual shares and debt.

CET 1 Ratio = [CET 1 Capital / RWAs]*100

This forms a part of the total CAR.

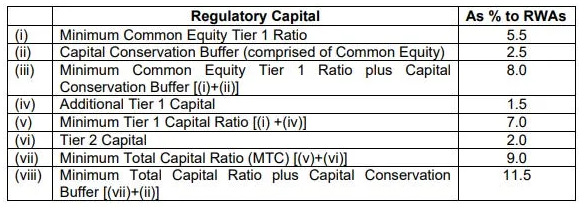

Capital Conservation Buffer (CCB) -

As per RBI & Basel 3 norms, these are the required capital buffers →

Capital Requirements

Capital Requirements

The last but not the least is the Leverage Ratio which measures the bank’s core capital (Tier 1) against its total exposure without risk weighting.

Leverage Ratio = [Tier 1 Capital/ Total Exposure]*100

Total Exposure includes both on-balance sheet exposures- loans, investments and advances.

Off-balance exposures — Letters of credit, guarantees, derivatives exposure.

Under Basel 3- 3% globally while RBI generally requires ~4.5% for Indian Banks.

Liquidity Requirements

All the topics covered were the basics but there are some other liquidity requirements which are necessary for banks to maintain.

Liquidity Coverage Ratio (LCR) — It is a Basel 3 requirement which makes a bank to hold a sufficient stock of High Quality Liquid Assets (HQLAs) to cover net cash outflows for 30 days under a stressed scenario.

LCR = [Stock of High Quality Liquid Assets (HQLAs) / Total Net Cash Outflows over 30 days]*100

HQLAs can be easily and immediately converted into cash with little/no loss of value like Cash Balances with RBI, Govt. Securities.

Total Net Cash Outflows (30 days) = Expected Cash Outflows- Expected Cash Inflows

Outflows: Withdrawals of deposits, drawdowns of credit lines.

Inflows: Loan repayments, maturing investments (up to a cap of 75% of outflows).

Under Basel 3- Banks required to maintain LCR >=100%

LCR ensures banks do not over leverage as the loans given out by banks are long term while CASA (Current Account- Savings Account) deposits can be short term with immediate requirements arising from the vast number of depositors.

Net Stable Funding Ratio (NSFR) — Requires banks to maintain stable funding profile in relation to the composition of their assets and off-balance sheet activities over one year horizon.

NSFR = [ (Available Stable Funding- ASF)/ (Required Stable Funding- RSF)]*100

Key Components of ASF — Funding sources expected to be reliable over the one-year horizon like Regulatory Capital (equity, Tier 1 and Tier 2 Capital), Long term deposits and long term borrowings with maturity greater than 1 year.

Key Components of RSF — Determined by liquidity characteristics & residual maturities of the bank’s assets and off balance sheet exposures. Assets are weighted according to their liquidity like Cash (0% weightage), Loan to retail customers (85% weightage) while Long term corporate loans (100% weightage).

NSFR should be >= 100% under Basel 3. This ensures banks have sufficient stable funding to support their long-term illiquid assets and activities.

Summary

To lend INR 100 →

Equity Requirement (Own Capital Required) — CAR+CCB — 11.5% of 100 = 11.50

Reserve Requirements (RBI) — Certain % of NDTL set aside- CRR + SLR — 4.5% + 18% = 22.5% of NDTL. To actually asses NDTL present with bank, we need to check the Credit to Deposit ratio which can be around 75% for healthy banks. So for lending 100, 133.33 would be required.

So reserve requirements = 22.5% of 133.33 = 30 INR

Hence to lend INR 100 — Nearly 30 INR is locked in reserves and additional equity of 11.50 needs to be raised.

Further understanding can be built by reading the Annual Reports of Banks which disclose all the above requirements plus additional reserves banks keep for prudency and fiscal health.

I will also write more on the P&L of a bank and the provisions created by the bank and the history behind the large NPAs which used to pull our banks in the previous decade in the upcoming articles.